I am asking John McDonnell the Labour MP for Hayes and Harlington to remind the Chancellor Rishi Sunak and Prime Minster Boris Johnson to use their persuasive skills to highlight and take a more holistic approach and attitude to the private rented sector and tackle issues which affect a Hayes landlords’ capability and capacity to strategically run an effective buy-to-let business.

For the last thirty years, the Government have passed responsibility of housing the masses from local authorities (i.e. council housing) to the estimated 1.5 million British buy-to-let landlords.

However, since 2015/16, Hayes landlords have faced increasing tax burdens as each year goes by, with the removal of mortgage interest rate relief on income tax (Section 24), the introduction of the 3 percent surcharge on stamp duty, and the reduction of the letting relief on capital gains tax.

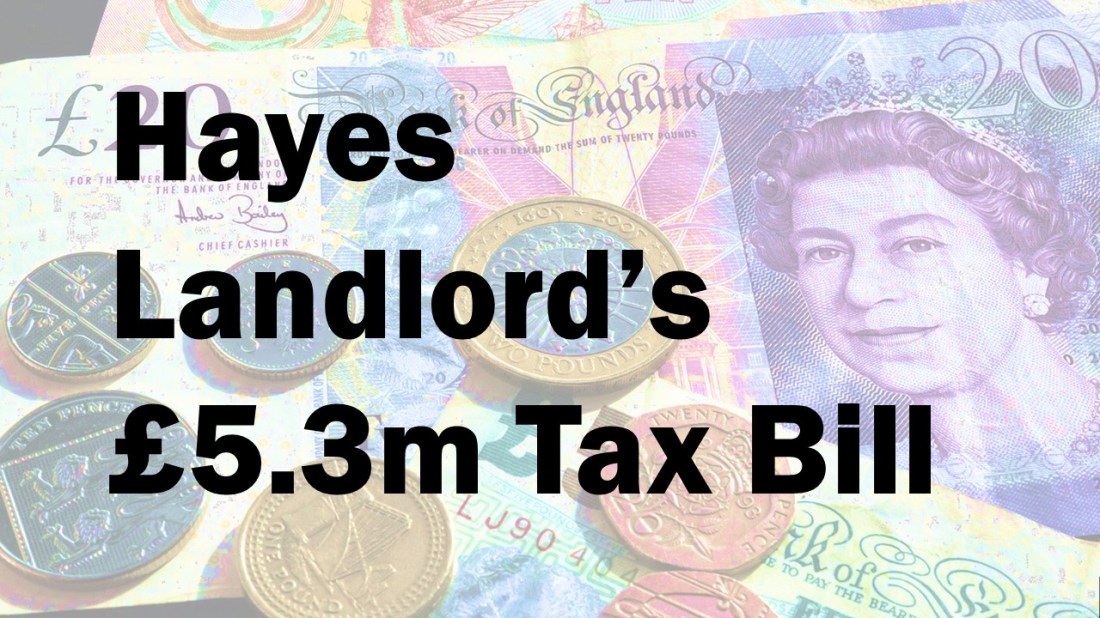

My research has calculated the total income tax contribution by 1,415 Hayes (UB3) private landlords in the tax year 2015/16 was £3,692,146

However, the eradication of higher rate mortgage interest relief (also known as Section 24) announced in 2015 by George Osborne has been estimated to add a further £1.9 billion nationally to landlord’s tax liability. Whilst raising money from landlords is an easy target, and the tax receipts attractive, it does make the landlords financial burden even heavier.

And by 2021/2, when the full extent of the Section 24 relief kicks in, that income tax liability will rise to £5,390,533

for those Hayes (UB3 landlords

This doesn’t even take into account additional liabilities such as Capital Gains Tax, the 3% additional duty on top of the prevailing Stamp Duty Land Tax and VAT.

Ambiguity and a lack of certainty is the foe of all investment, which has been seen with Brexit. Now, just as things are starting to get rosy in Q1 with the pent-up demand released with the ‘Boris Bounce’, the last thing we need as a ‘collective’ property industry is for the Government to see us landlords as a constant cash cow. This new Tory government must acknowledge the value the majority of private landlords offer by housing in excess of 9.45 million people in the country.

Westminster needs to take a balanced approach to the significant issues of possession (especially with the impeding removal of section 21 evictions), taxation and all rental properties needing to be at least an ‘E’ energy efficiency rating, to connect the value the private rented sector offers the country by effectively housing over a fifth of the population and avoid unintentional consequences by making renting a private rented property harder for tenants … because, it’s not financially viable to buy (or retain) a buy-to-let property with the way things are going against the landlord.